UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

FORM 6-K

REPORT OF FOREIGN PRIVATE ISSUER

PURSUANT TO RULE 13a-16 OR 15d-16

UNDER THE SECURITIES EXCHANGE ACT OF 1934

For the month of March 2022

Commission File Number: 001-40451

DLocal Limited

(Exact name of registrant as specified in its charter)

Dr. Luis Bonavita 1294

Montevideo

Uruguay 11300

+1 (424) 392-7437

(Address of principal executive office)

Indicate by check mark whether the registrant files or will file annual reports under cover of Form 20-F or Form 40-F:

Form 20-F ☒ Form 40-F ☐

Indicate by check mark if the registrant is submitting the Form 6-K in paper as permitted by Regulation S-T Rule 101(b)(1):

Yes ☐ No ☒

Indicate by check mark if the registrant is submitting the Form 6-K in paper as permitted by Regulation S-T Rule 101(b)(7):

Yes ☐ No ☒

TABLE OF CONTENTS

EXHIBIT

|

|

|

99.1 |

|

Press release dated March 14, 2021 - DLocal Limited Reports 2021 Fourth Quarter and Full Year Financial Results |

|

|

|

99.2 |

|

DLocal Limited Consolidated Financial Statements as of December 31, 2021 and 2020 and for the three years in the period ended December 31, 2021 |

|

|

|

99.3 |

|

Annual Report 2021 - dLocal Reports 2021 Fourth Quarter & full year Financial results |

|

|

|

99.4 |

|

dLocal Q4 & FY2021 Earnings Presentation |

SIGNATURE

Pursuant to the requirements of the Securities Exchange Act of 1934, the registrant has duly caused this report to be signed on its behalf by the undersigned, thereunto duly authorized.

|

DLocal Limited |

|

|

|

|

|

|

|

By: |

/s/ Diego Cabrera Canay |

|

|

Name: |

Diego Cabrera Canay |

|

|

Title: |

Chief Financial Officer |

|

Date: March 15, 2022

dLocal Limited Reports 2021 Fourth Quarter and Full Year Financial Results

Full Year 2021

US$6.0 billion Total Payment Volume, up 193% year-over-year

Revenues of US$244.1 million, up 134% year-over-year

219% Net Retention Rate

41% Adj EBITDA Margin

Fourth Quarter 2021

US$1.9 billion Total Payment Volume, up 145% year-over-year

Revenues of US$76.3 million, up 120% year-over-year

198% Net Retention Rate

38% Adj EBITDA Margin

dLocal reports in US dollars and in accordance with IFRS as issued by the IASB

Montevideo, Uruguay March 14, 2022 — DLocal Limited (“dLocal”, “we”, “us”, and “our”) (NASDAQ:DLO), a technology- first payments platform today announced its financial results for the fourth quarter and full year ended December 31, 2021.

“Dear Customers, Partners and Shareholders,

Thank you for your continued support and trust. We started our journey a little over 6 years ago and we are proud of what we have accomplished till date, but we are literally just getting started. We became Uruguay’s first unicorn and debuted as a public company in June 2021. This has set the beginning of a new chapter for dLocal but our priorities and values have not changed. We remain humble and focused as we continue to turn the complex into simple for our merchants and we continue to redefine the online payments experience in emerging markets.

Our vision is to build a network of payments infrastructure such that making or receiving a payment in the emerging markets to and from anywhere in the world is as simple as sending an email. We are doing this country by country and payment method by payment method. Today, we are in 35 countries and connected to 700+ payment methods.

We started in Uruguay but we were born global. Our first significant win was with a U.S. based enterprise merchant that needed us to solve a local payments problem in Brazil. We then realized that the problem we were solving in Brazil also existed in many other places, so we expanded to Latin America. Our merchants faced the same challenges in the rest of the world, so we expanded to Africa and Asia. We continue to expand our footprint in emerging markets.

2021 was a record year. Our TPV almost tripled in 2021, surpassing the US$6 billion threshold, increasing by 193% year-over-year. Revenues for the year reached US$244 million, a 134% year-over-year growth, with an Adjusted EBITDA margin of 41%, compared to 40% in 2020. We continued to make investments in infrastructure and people to support our expansion strategy. These results were supported by the continued growth from both existing and new merchants using our platform.

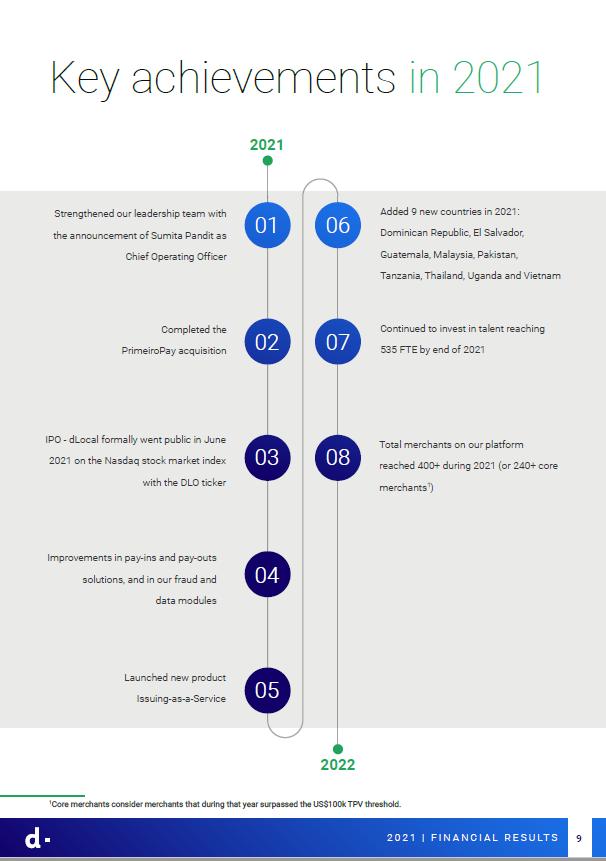

We serve online global merchants who are looking to do business in multiple geographies. We are agnostic to industry verticals and have built a diversified business across geographies, sectors, and products. We remain committed to agile decision making and providing tailored solutions for our merchants to help them achieve their growth plans in emerging markets. We are a revenue enabler for our clients, and we grow when they grow. Total merchants on our platform have grown steadily from 300+ in 2020 to 400+ in 2021, and we have a robust sales pipeline ahead. This pipeline is supported mainly by the rapid expansion and ramp up of online merchants, by the consistent growth of the global creator economy and by the increased relevance of digital marketing worldwide, which are not limited by geographic boundaries. During the year, we have seen new companies emerge and establish dominance very quickly, and we expect this trend to continue moving forward.

We have continued to expand our footprint in emerging markets, launching operations in nine new countries (six of them outside Latin America) during 2021, bringing the total number of countries in which we make our services available to 35.

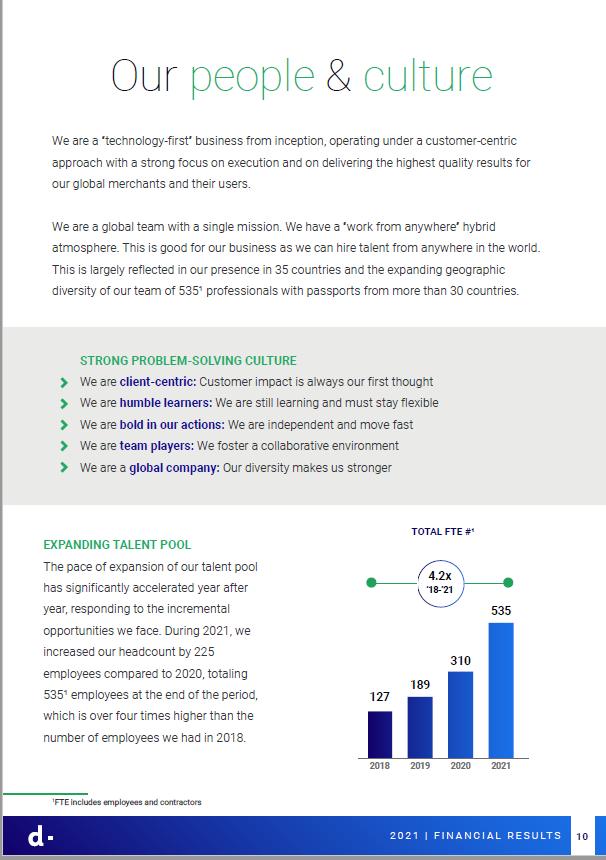

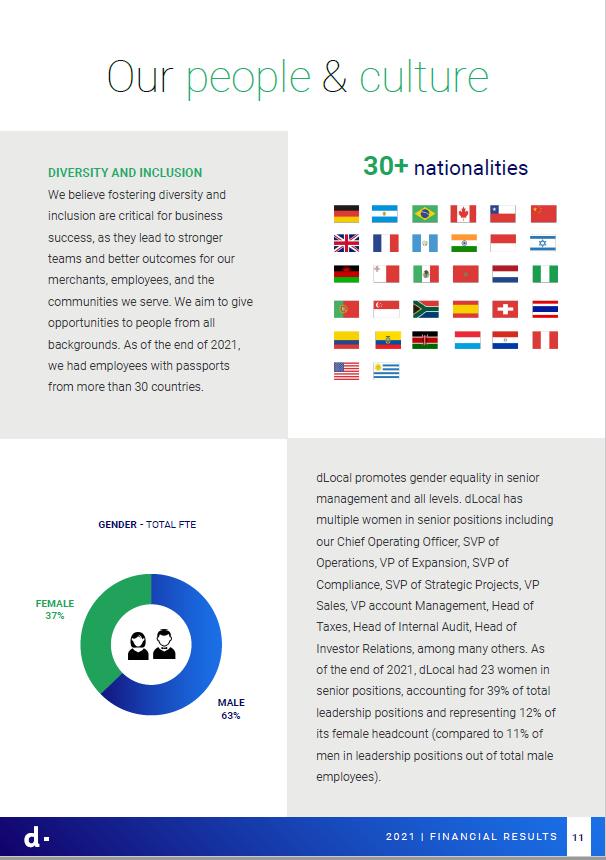

Our culture and our people make us who we are. We pride ourselves on our growth mindset and our ability to be flexible, fast and focused. We believe a high-quality team is the cornerstone for our long-term success. Throughout 2021, we have continued to invest in adding talent, with complementary and diverse backgrounds, reaching 535 employees by the year end, a 73% year-over-year increase.

We have built our company with a long-term vision, and as we look ahead, we are very excited with the opportunities we foresee. We remain focused on creating value for our merchants and our shareholders, and we believe we are in a unique position to capture these opportunities and to continue delivering profitable growth and strong financial results as the years go by,” said Sebastian Kanovich.

Fourth Quarter and Full Year 2021 Financial Highlights

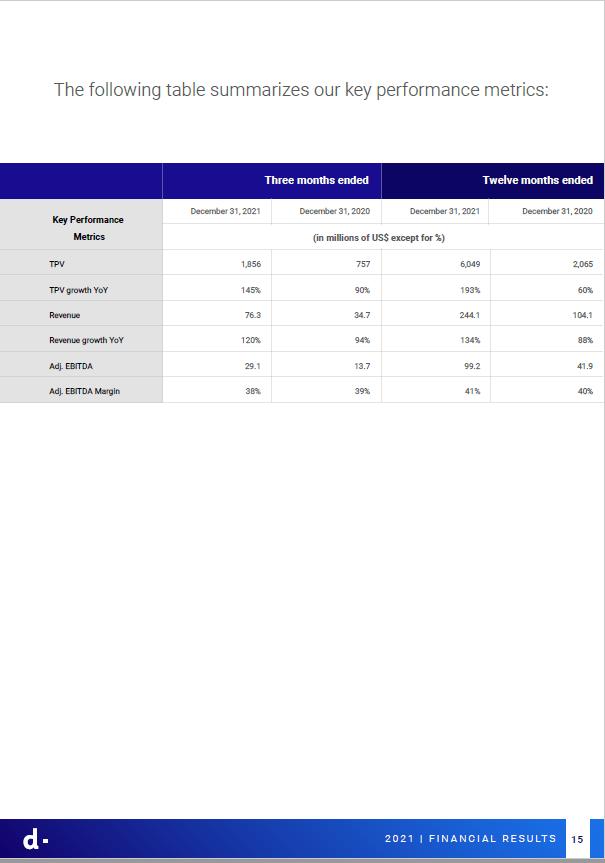

The following table summarizes our key performance metrics:

|

Three months ended |

|

Twelve months ended |

||||

December 31, 2021 |

|

December 31, 2020 |

|

December 31, 2021 |

|

December 31, 2020 |

|

(in millions of US$ except for %) |

|||||||

Key Performance Metrics |

|

|

|

|

|

|

|

TPV |

1,856 |

|

757 |

|

6,049 |

|

2,065 |

TPV growth YoY |

145% |

|

90% |

|

193% |

|

60% |

Revenue |

76.3 |

|

34.7 |

|

244.1 |

|

104.1 |

Revenue growth YoY |

120% |

|

94% |

|

134% |

|

88% |

Adj. EBITDA |

29.1 |

|

13.7 |

|

99.2 |

|

41.9 |

Adj. EBITDA Margin |

38% |

|

39% |

|

41% |

|

40% |

Fourth Quarter and Full Year 2021 Business Highlights

1 Including the effect in 2019 of a warrant with a merchant (valued at US$4.3 million, which was a contra-revenue for such year), the NRR would have been 171%.

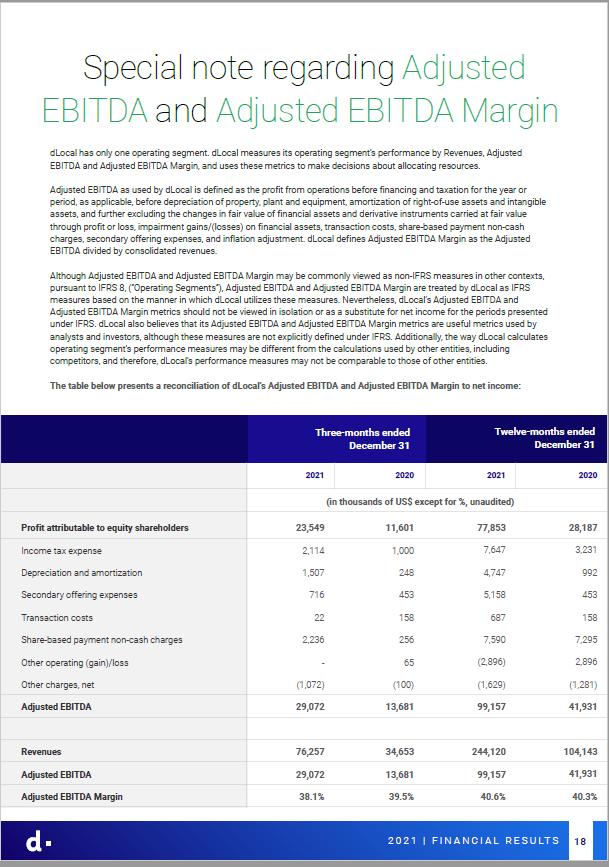

Special Note Regarding Adjusted EBITDA and Adjusted EBITDA Margin

dLocal has only one operating segment. dLocal measures its operating segment’s performance by Revenues, Adjusted EBITDA and Adjusted EBITDA Margin, and uses these metrics to make decisions about allocating resources.

Adjusted EBITDA as used by dLocal is defined as the profit from operations before financing and taxation for the year or period, as applicable, before depreciation of property, plant and equipment, amortization of right-of-use assets and intangible assets, and further excluding the changes in fair value of financial assets and derivative instruments carried at fair value through profit or loss, impairment gains/(losses) on financial assets, transaction costs, share-based payment non-cash charges, secondary offering expenses, and inflation adjustment. dLocal defines Adjusted EBITDA Margin as the Adjusted EBITDA divided by consolidated revenues.

Although Adjusted EBITDA and Adjusted EBITDA Margin may be commonly viewed as non-IFRS measures in other contexts, pursuant to IFRS 8, (“Operating Segments”), Adjusted EBITDA and Adjusted EBITDA Margin are treated by dLocal as IFRS measures based on the manner in which dLocal utilizes these measures. Nevertheless, dLocal’s Adjusted EBITDA and Adjusted EBITDA Margin metrics should not be viewed in isolation or as a substitute for net income for the periods presented under IFRS. dLocal also believes that its Adjusted EBITDA and Adjusted EBITDA Margin metrics are useful metrics used by analysts and investors, although these measures are not explicitly defined under IFRS. Additionally, the way dLocal calculates operating segment’s performance measures may be different from the calculations used by other entities, including competitors, and therefore, dLocal’s performance measures may not be comparable to those of other entities.

The table below presents a reconciliation of dLocal’s Adjusted EBITDA and Adjusted EBITDA Margin to net income:

|

Three-months ended December 31 |

Twelve-months ended December 31 |

||

|

2021 |

2020 |

2021 |

2020 |

Profit for the period |

23,549 |

11,601 |

77,853 |

28,187 |

Income tax expense |

2,114 |

1,000 |

7,647 |

3,231 |

Depreciation and amortization |

1,507 |

248 |

4,747 |

992 |

Secondary offering expenses |

716 |

453 |

5,158 |

453 |

Transaction costs |

22 |

158 |

687 |

158 |

Share-based payment non-cash charges |

2,236 |

256 |

7,590 |

7,295 |

Other operating (gain)/loss |

- |

65 |

(2,896) |

2,896 |

Other charges, net |

(1,072) |

(100) |

(1,629) |

(1,281) |

Adjusted EBITDA |

29,072 |

13,681 |

99,157 |

41,931 |

|

|

|

|

|

Revenues |

76,257 |

34,653 |

244,120 |

104,143 |

Adjusted EBITDA |

29,072 |

13,681 |

99,157 |

41,931 |

Adjusted EBITDA Margin |

38.1% |

39.5% |

40.6% |

40.3% |

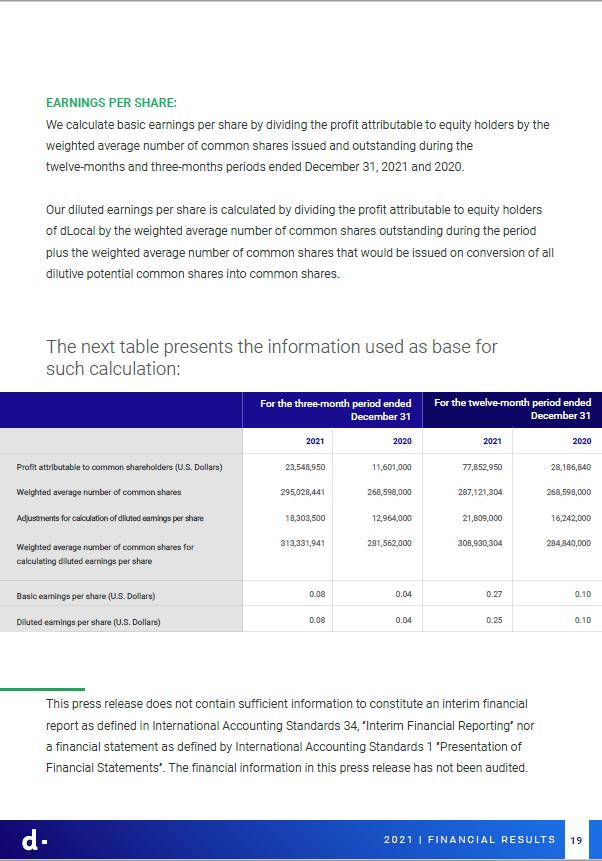

Earnings per share:

We calculate basic earnings per share by dividing the profit attributable to equity holders by the weighted average number of common shares issued and outstanding during the twelve-months and three-months periods ended December 31, 2021 and 2020.

Our diluted earnings per share is calculated by dividing the profit attributable to equity holders of dLocal by the weighted average number of common shares outstanding during the period plus the weighted average number of common shares that would be issued on conversion of all dilutive potential common shares into common shares.

The next table presents the information used as base for such calculation

|

For the three-month period ended December 31 |

For the twelve-month period ended December 31 |

||

|

2021 |

2020 |

2021 |

2020 |

Profit attributable to common shareholders (U.S. Dollars) |

23,548,950 |

11,601,000 |

77,852,950 |

28,186,840 |

Weighted average number of common shares |

295,028,441 |

268,598,000 |

287,121,304 |

268,598,000 |

Adjustments for calculation of diluted earnings per share |

18,303,500 |

12,964,000 |

21,809,000 |

16,242,000 |

Weighted average number of common shares for calculating diluted earnings per share |

313,331,941 |

281,562,000 |

308,930,304 |

284,840,000 |

Basic earnings per share |

0.08 |

0.04 |

0.27 |

0.10 |

Diluted earnings per share |

0.08 |

0.04 |

0.25 |

0.10 |

This press release does not contain sufficient information to constitute an interim financial report as defined in International Accounting Standards 34, “Interim Financial Reporting” nor a financial statement as defined by International Accounting Standards 1 “Presentation of Financial Statements”. The financial information in this press release has not been audited.

Conference Call and Webcast

dLocal’s management team will host a conference call and audio webcast on March 15, 2022 at 8:30 a.m. Eastern Time. The conference call may be accessed by dialing (888) 705-0197/ (409) 981-0764 (Conference ID – 3689961 –) and requesting inclusion in the call for dLocal.

The live conference call can be accessed via audio webcast at the investor relations section of dLocal’s website, at https://investor.dlocal.com/. An archive of the webcast will be available for a year following the conclusion of the conference call. The investor presentation will also be filed on EDGAR at www.sec.gov.

About dLocal

dLocal powers local payments in emerging markets, connecting global enterprise merchants with billions of emerging market consumers in 35 countries across APAC, the Middle East, Latin America, and Africa. Through the “One dLocal” platform (one direct API, one platform, and one contract), global companies can accept payments, send pay-outs and settle funds globally without the need to manage separate pay-in and pay-out processors, set up numerous local entities, and integrate multiple acquirers and payment methods in each market.

Definition of Selected Operational Metrics

“API” means application programming interface, which is a general term for programming techniques that are available for software developers when they integrate with a particular service or application. In the payments industry, APIs are usually provided by any party participating in the money flow (such as payment gateways, processors, service providers) to facilitate the money transfer process.

“Enterprise Global Merchants” means merchants with at least US$6 million of annual TPV processed through our platform.

“Local payment methods” refers to any payment method that is processed in the country where the end user of the merchant sending or receiving payments is located, which include credit and debit cards, cash payments, bank transfers, mobile money, and digital wallets.

“NRR” means net revenue retention rate, which is the U.S. dollar-based measure of retention and growth of our merchants. We calculate the NRR of a period by dividing the current period revenue by the prior period revenue. The prior period revenue is the revenue billed by us to all of our merchant customers in the corresponding period for the prior fiscal year. The current period revenue is the revenue billed by us in the corresponding period for the current fiscal year to the same merchant customers included in the calculation of the prior period revenue. Current period revenue includes any upsells and cross sells of products, geographies, and payment methods to such merchant customers, and is net of any contractions or attrition, but excludes revenue from new customers on-boarded during the last 12 months.

“Pay-in” means a payment transaction whereby dLocal’s merchant customers receive payment from their customers.

“Pay-out” means a payment transaction whereby dLocal disburses money in local currency to the business partners or customers of dLocal’s merchant customers.

“Revenue from New Merchants”: means the revenue billed by us to merchant customers that we did not bill revenues in the same quarter (or period) of the prior year.

“Revenue from Existing Merchants”: means the revenue billed by us in the last twelve months to the merchant customers that we billed revenue in the same quarter (or period) of the prior year.

Forward Looking Statements

This press release contains certain forward-looking statements. These forward-looking statements convey dLocal’s current expectations or forecasts of future events. Forward-looking statements regarding dLocal involve known and unknown risks, uncertainties and other factors that may cause dLocal’s actual results, performance or achievements to be materially different from any future results, performances or achievements expressed or implied by the forward-looking statements. Certain of these risks and uncertainties are described in the “Risk Factors,” “Forward-Looking Statements” and “Cautionary Note Regarding Forward-Looking Statements” sections of dLocal’s filings with the U.S. Securities and Exchange Commission. Unless required by law, dLocal undertakes no obligation to publicly update or revise any forward-looking statements to reflect circumstances or events after the date hereof.

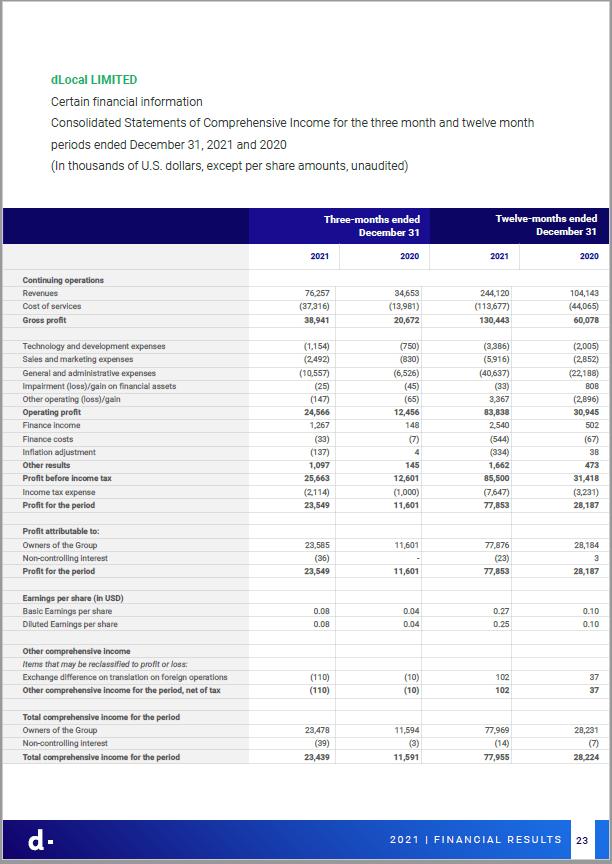

DLocal Limited

Certain financial information

Consolidated Statements of Comprehensive Income for the three month and twelve month periods ended December 31, 2021 and 2020

(In thousands of U.S. dollars, except per share amounts, unaudited)

|

|

Three-months ended December 31 |

|

Twelve-months ended December 31 |

|

||||

|

|

2021 |

|

2020 |

|

2021 |

|

2020 |

|

Continuing operations |

|

|

|

|

|

|

|

|

|

Revenues |

|

76,257 |

|

34,653 |

|

244,120 |

|

104,143 |

|

Cost of services |

|

(37,316) |

|

(13,981) |

|

(113,677) |

|

(44,065) |

|

Gross profit |

|

38,941 |

|

20,672 |

|

130,443 |

|

60,078 |

|

|

|

|

|

|

|

|

|

|

|

Technology and development expenses |

|

(1,154) |

|

(750) |

|

(3,386) |

|

(2,005) |

|

Sales and marketing expenses |

|

(2,492) |

|

(830) |

|

(5,916) |

|

(2,852) |

|

General and administrative expenses |

|

(10,557) |

|

(6,526) |

|

(40,637) |

|

(22,188) |

|

Impairment (loss)/gain on financial assets |

|

(25) |

|

(45) |

|

(33) |

|

808 |

|

Other operating (loss)/gain |

|

(147) |

|

(65) |

|

3,367 |

|

(2,896) |

|

Operating profit |

|

24,566 |

|

12,456 |

|

83,838 |

|

30,945 |

|

Finance income |

|

1,267 |

|

148 |

|

2,540 |

|

502 |

|

Finance costs |

|

(33) |

|

(7) |

|

(544) |

|

(67) |

|

Inflation adjustment |

|

(137) |

|

4 |

|

(334) |

|

38 |

|

Other results |

|

1,097 |

|

145 |

|

1,662 |

|

473 |

|

Profit before income tax |

|

25,663 |

|

12,601 |

|

85,500 |

|

31,418 |

|

Income tax expense |

|

(2,114) |

|

(1,000) |

|

(7,647) |

|

(3,231) |

|

Profit for the period |

|

23,549 |

|

11,601 |

|

77,853 |

|

28,187 |

|

|

|

|

|

|

|

|

|

|

|

Profit attributable to: |

|

|

|

|

|

|

|

|

|

Owners of the Group |

|

23,585 |

|

11,601 |

|

77,876 |

|

28,184 |

|

Non-controlling interest |

|

(36) |

|

- |

|

(23) |

|

3 |

|

Profit for the period |

|

23,549 |

|

11,601 |

|

77,853 |

|

28,187 |

|

|

|

|

|

|

|

|

|

|

|

Earnings per share (in USD) |

|

|

|

|

|

|

|

|

|

Basic Earnings per share |

|

0.08 |

|

0.04 |

|

0.27 |

|

0.10 |

|

Diluted Earnings per share |

|

0.08 |

|

0.04 |

|

0.25 |

|

0.10 |

|

|

|

|

|

|

|

|

|

|

|

Other comprehensive income |

|

|

|

|

|

|

|

|

|

Items that may be reclassified to profit or loss: |

|

|

|

|

|

|

|

|

|

Exchange difference on translation on foreign operations |

|

(110) |

|

(10) |

|

102 |

|

37 |

|

Other comprehensive income for the period, net of tax |

|

(110) |

|

(10) |

|

102 |

|

37 |

|

|

|

|

|

|

|

|

|

|

|

Total comprehensive income for the period |

|

|

|

|

|

|

|

|

|

Owners of the Group |

|

23,478 |

|

11,594 |

|

77,969 |

|

28,231 |

|

Non-controlling interest |

|

(39) |

|

(3) |

|

(14) |

|

(7) |

|

Total comprehensive income for the period |

|

23,439 |

|

11,591 |

|

77,955 |

|

28,224 |

|

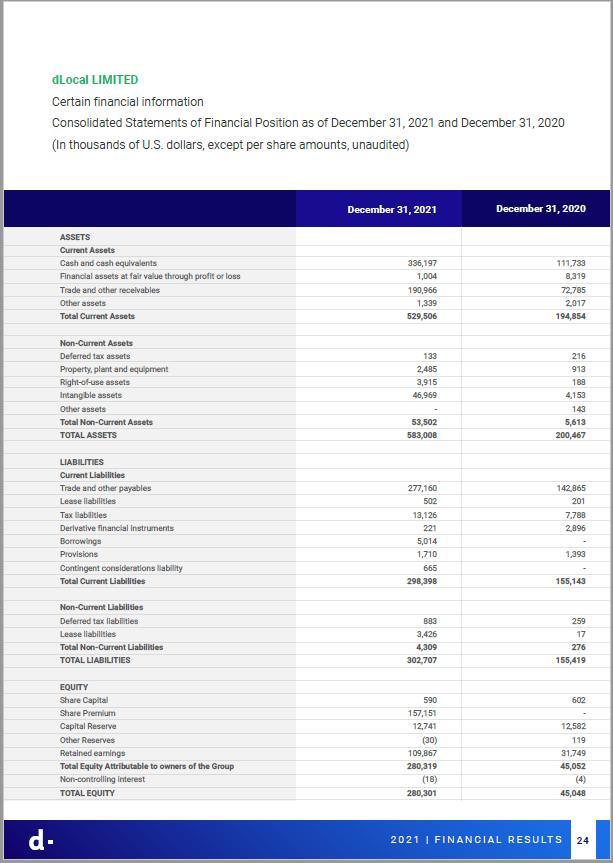

DLocal Limited

Certain financial information

Consolidated Statements of Financial Position as of December 31, 2021 and December 31, 2020

(In thousands of U.S. dollars, except per share amounts, unaudited)

|

|

|

December 31, 2021 |

|

December 31, 2020 |

ASSETS |

|

|

|

|

|

Current Assets |

|

|

|

|

|

Cash and cash equivalents |

|

|

336,197 |

|

111,733 |

Financial assets at fair value through profit or loss |

|

|

1,004 |

|

8,319 |

Trade and other receivables |

|

|

190,966 |

|

72,785 |

Other assets |

|

|

1,339 |

|

2,017 |

Total Current Assets |

|

|

529,506 |

|

194,854 |

|

|

|

|

|

|

Non-Current Assets |

|

|

|

|

|

Deferred tax assets |

|

|

133 |

|

216 |

Property, plant and equipment |

|

|

2,485 |

|

913 |

Right-of-use assets |

|

|

3,915 |

|

188 |

Intangible assets |

|

|

46,969 |

|

4,153 |

Other assets |

|

|

- |

|

143 |

Total Non-Current Assets |

|

|

53,502 |

|

5,613 |

TOTAL ASSETS |

|

|

583,008 |

|

200,467 |

|

|

|

|

|

|

LIABILITIES |

|

|

|

|

|

Current Liabilities |

|

|

|

|

|

Trade and other payables |

|

|

277,160 |

|

142,865 |

Lease liabilities |

|

|

502 |

|

201 |

Tax liabilities |

|

|

13,126 |

|

7,788 |

Derivative financial instruments |

|

|

221 |

|

2,896 |

Borrowings |

|

|

5,014 |

|

- |

Provisions |

|

|

1,710 |

|

1,393 |

Contingent considerations liability |

|

|

665 |

|

- |

Total Current Liabilities |

|

|

298,398 |

|

155,143 |

|

|

|

|

|

|

Non-Current Liabilities |

|

|

|

|

|

Deferred tax liabilities |

|

|

883 |

|

259 |

Lease liabilities |

|

|

3,426 |

|

17 |

Total Non-Current Liabilities |

|

|

4,309 |

|

276 |

TOTAL LIABILITIES |

|

|

302,707 |

|

155,419 |

|

|

|

|

|

|

EQUITY |

|

|

|

|

|

Share Capital |

|

|

590 |

|

602 |

Share Premium |

|

|

157,151 |

|

- |

Capital Reserve |

|

|

12,741 |

|

12,582 |

Other Reserves |

|

|

(30) |

|

119 |

Retained earnings |

|

|

109,867 |

|

31,749 |

Total Equity Attributable to owners of the Group |

|

|

280,319 |

|

45,052 |

Non-controlling interest |

|

|

(18) |

|

(4) |

TOTAL EQUITY |

|

|

280,301 |

|

45,048 |

dLocal was incorporated on February 10, 2021, as a Cayman Islands exempted company with limited liability, duly registered with the Cayman Islands Registrar of Companies. The contribution of dLocal Group Limited (a limited liability company incorporated in Malta, the former holding entity or “dLocal Malta”) shares to dLocal was the Cayman Islands company has been finalized as of April 14, 2021. Until the contribution of dLocal Malta shares to it, dLocal had not commenced operations, consequently the historical information previous to that date presented in here corresponds to dLocal Malta, our predecessor. This reorganization was done, among other things, to facilitate the initial public offering of the Group. dLocal had no prior assets, holdings or operations.

Investor Relations Contact:

investor@dlocal.com

Media Contact:

marketing@dlocal.com

DLocal Limited

Consolidated Financial Statements

as of December 31, 2021 and 2020

and for the three years in the period ended December 31, 2021

INDEX TO CONSOLIDATED FINANCIAL STATEMENTS

|

Page |

|

|

Consolidated Financial Statements as of December 31, 2021 and 2020 and for the three years in the period ended December 31, 2021 |

|

Report of Independent Registered Public Accounting Firm (PCAOB ID1349) |

- |

Consolidated Statements of Comprehensive Income for the years ended December 31, 2021, 2020 and 2019 |

1 |

Consolidated Statements of Financial Position at December 31, 2021 and 2020 |

2 |

Consolidated Statements of Changes in Equity for the years ended December 31, 2021, 2020 and 2019 |

3 |

Consolidated Statements of Cash Flows for the years ended December 31, 2021, 2020 and 2019 |

4 |

5 |

Report of Independent Registered Public Accounting Firm

To the Board of Directors and Shareholders of DLocal Limited

Opinion on the Financial Statements

We have audited the accompanying consolidated statements of financial position of DLocal Limited and its subsidiaries (the “Company”) as of December 31, 2021 and 2020, and the related consolidated statements of comprehensive income, changes in equity and cash flows for each of the three years in the period ended December 31, 2021, including the related notes (collectively referred to as the “consolidated financial statements”). In our opinion, the consolidated financial statements present fairly, in all material respects, the financial position of the Company as of December 31, 2021 and 2020, and the results of its operations and its cash flows for each of the three years in the period ended December 31, 2021 in conformity with International Financial Reporting Standards as issued by the International Accounting Standards Board.

Basis for Opinion

These consolidated financial statements are the responsibility of the Company’s management. Our responsibility is to express an opinion on the Company’s consolidated financial statements based on our audits. We are a public accounting firm registered with the Public Company Accounting Oversight Board (United States) (PCAOB) and are required to be independent with respect to the Company in accordance with the U.S. federal securities laws and the applicable rules and regulations of the Securities and Exchange Commission and the PCAOB.

We conducted our audits of these consolidated financial statements in accordance with the standards of the PCAOB. Those standards require that we plan and perform the audit to obtain reasonable assurance about whether the consolidated financial statements are free of material misstatement, whether due to error or fraud.

Our audits included performing procedures to assess the risks of material misstatement of the consolidated financial statements, whether due to error or fraud, and performing procedures that respond to those risks. Such procedures included examining, on a test basis, evidence regarding the amounts and disclosures in the consolidated financial statements. Our audits also included evaluating the accounting principles used and significant estimates made by management, as well as evaluating the overall presentation of the consolidated financial statements. We believe that our audits provide a reasonable basis for our opinion.

/s/ Price Waterhouse & Co. S.R.L.

Gustavo Ariel Vidan (Partner)

Autonomous City of Buenos Aires, Argentina

March 15, 2022

We have served as the Company’s auditor since 2020.

DLocal Limited

Consolidated Statements of Comprehensive Income

Years ended December 31, 2021, 2020 and 2019

(All amounts in thousands of U.S. Dollars except share data or as otherwise indicated)

|

|

Notes |

|

For the Year Ended December 31, |

|

|||||||||

|

|

|

|

2021 |

|

|

2020 |

|

|

2019 |

|

|||

Continuing operations |

|

|

|

|

|

|

|

|

|

|

|

|||

Revenues |

|

6 |

|

|

244,120 |

|

|

|

104,143 |

|

|

|

55,289 |

|

Cost of services |

|

6 |

|

|

(113,677 |

) |

|

|

(44,065 |

) |

|

|

(19,413 |

) |

Gross profit |

|

|

|

|

130,443 |

|

|

|

60,078 |

|

|

|

35,876 |

|

Technology and development expenses |

|

7 |

|

|

(3,386 |

) |

|

|

(2,005 |

) |

|

|

(1,347 |

) |

Sales and marketing expenses |

|

8 |

|

|

(5,916 |

) |

|

|

(2,852 |

) |

|

|

(2,057 |

) |

General and administrative expenses |

|

8 |

|

|

(40,637 |

) |

|

|

(22,188 |

) |

|

|

(14,101 |

) |

Impairment (loss)/gain on financial assets |

|

16 |

|

|

(33 |

) |

|

|

808 |

|

|

|

(807 |

) |

Other operating gain/(loss) |

|

24 |

|

|

3,367 |

|

|

|

(2,896 |

) |

|

|

— |

|

Operating profit |

|

|

|

|

83,838 |

|

|

|

30,945 |

|

|

|

17,564 |

|

Finance income |

|

11 |

|

|

2,540 |

|

|

|

502 |

|

|

|

279 |

|

Finance costs |

|

11 |

|

|

(544 |

) |

|

|

(67 |

) |

|

|

(30 |

) |

Inflation adjustment |

|

11 |

|

|

(334 |

) |

|

|

38 |

|

|

|

10 |

|

Other results |

|

|

|

|

1,662 |

|

|

|

473 |

|

|

|

259 |

|

Profit before income tax |

|

|

|

|

85,500 |

|

|

|

31,418 |

|

|

|

17,823 |

|

Income tax expense |

|

12 |

|

|

(7,647 |

) |

|

|

(3,231 |

) |

|

|

(2,221 |

) |

Profit for the year |

|

|

|

|

77,853 |

|

|

|

28,187 |

|

|

|

15,602 |

|

Profit attributable to: |

|

|

|

|

|

|

|

|

|

|

|

|||

Owners of the Group |

|

|

|

|

77,876 |

|

|

|

28,184 |

|

|

|

15,602 |

|

Non-controlling interest |

|

|

|

|

(23 |

) |

|

|

3 |

|

|

|

— |

|

Profit for the year |

|

|

|

|

77,853 |

|

|

|

28,187 |

|

|

|

15,602 |

|

Earnings per share |

|

|

|

|

|

|

|

|

|

|

|

|||

Basic Earnings per share |

|

13 |

|

|

0.27 |

|

|

|

0.10 |

|

|

|

0.06 |

|

Diluted Earnings per share |

|

13 |

|

|

0.25 |

|

|

|

0.10 |

|

|

|

0.05 |

|

Other comprehensive Income |

|

|

|

|

|

|

|

|

|

|

|

|||

Items that may be reclassified to profit or loss: |

|

|

|

|

|

|

|

|

|

|

|

|||

Exchange difference on translation on foreign operations |

|

|

|

|

102 |

|

|

|

37 |

|

|

|

27 |

|

Other comprehensive income for the year, net of tax |

|

|

|

|

102 |

|

|

|

37 |

|

|

|

27 |

|

Total comprehensive income for the year |

|

|

|

|

77,955 |

|

|

|

28,224 |

|

|

|

15,629 |

|

Total comprehensive income for the year is attributable to: |

|

|

|

|

|

|

|

|

|

|

|

|||

Owners of the Group |

|

|

|

|

77,969 |

|

|

|

28,231 |

|

|

|

15,629 |

|

Non-controlling interest |

|

|

|

|

(14 |

) |

|

|

(7 |

) |

|

|

— |

|

Total comprehensive income for the year |

|

|

|

|

77,955 |

|

|

|

28,224 |

|

|

|

15,629 |

|

The accompanying notes are an integral part of these consolidated financial statements.

1

DLocal Limited

Consolidated Statements of Financial Position

At December 31, 2021 and 2020

(All amounts in thousands of U.S. Dollars except share data or as otherwise indicated)

|

|

Notes |

|

December 31, |

|

|

December 31, |

|

||

ASSETS |

|

|

|

|

|

|

|

|

||

Current Assets |

|

|

|

|

|

|

|

|

||

Cash and cash equivalents |

|

14 |

|

|

336,197 |

|

|

|

111,733 |

|

Financial assets at fair value through profit or loss |

|

15 |

|

|

1,004 |

|

|

|

8,319 |

|

Trade and other receivables |

|

16 |

|

|

190,966 |

|

|

|

72,785 |

|

Other assets |

|

17 |

|

|

1,339 |

|

|

|

2,017 |

|

Total Current Assets |

|

|

|

|

529,506 |

|

|

|

194,854 |

|

Non-Current Assets |

|

|

|

|

|

|

|

|

||

Deferred tax assets |

|

12 |

|

|

133 |

|

|

|

216 |

|

Property, plant and equipment |

|

18 |

|

|

2,485 |

|

|

|

913 |

|

Right-of-use assets |

|

19 |

|

|

3,915 |

|

|

|

188 |

|

Intangible assets |

|

20 |

|

|

46,969 |

|

|

|

4,153 |

|

Other assets |

|

17 |

|

- |

|

|

|

143 |

|

|

Total Non-Current Assets |

|

|

|

|

53,502 |

|

|

|

5,613 |

|

TOTAL ASSETS |

|

|

|

|

583,008 |

|

|

|

200,467 |

|

LIABILITIES |

|

|

|

|

|

|

|

|

||

Current Liabilities |

|

|

|

|

|

|

|

|

||

Trade and other payables |

|

21 |

|

|

277,160 |

|

|

|

142,865 |

|

Borrowings |

|

22 |

|

|

5,014 |

|

|

|

— |

|

Lease liabilities |

|

19 |

|

|

502 |

|

|

|

201 |

|

Tax liabilities |

|

23 |

|

|

13,126 |

|

|

|

7,788 |

|

Derivative financial instruments |

|

24 |

|

|

221 |

|

|

|

2,896 |

|

Provisions |

|

25 |

|

|

1,710 |

|

|

|

1,393 |

|

Contingent consideration liability |

|

20 |

|

|

665 |

|

|

|

— |

|

Total Current Liabilities |

|

|

|

|

298,398 |

|

|

|

155,143 |

|

Non-Current Liabilities |

|

|

|

|

|

|

|

|

||

Deferred tax liabilities |

|

12 |

|

|

883 |

|

|

|

259 |

|

Lease liabilities |

|

19 |

|

|

3,426 |

|

|

|

17 |

|

Total Non-Current Liabilities |

|

|

|

|

4,309 |

|

|

|

276 |

|

TOTAL LIABILITIES |

|

|

|

|

302,707 |

|

|

|

155,419 |

|

EQUITY |

|

|

|

|

|

|

|

|

||

Share Capital |

|

13 |

|

|

590 |

|

|

|

602 |

|

Share Premium |

|

13 |

|

|

157,151 |

|

|

|

— |

|

Capital Reserve |

|

13 |

|

|

12,741 |

|

|

|

12,582 |

|

Other Reserves |

|

13 |

|

|

(30 |

) |

|

|

119 |

|

Retained earnings |

|

13 |

|

|

109,867 |

|

|

|

31,749 |

|

Total Equity Attributable to owners of the Group |

|

|

|

|

280,319 |

|

|

|

45,052 |

|

Non-controlling interest |

|

|

|

|

(18 |

) |

|

|

(4 |

) |

TOTAL EQUITY |

|

|

|

|

280,301 |

|

|

|

45,048 |

|

The accompanying notes are an integral part of these consolidated financial statements.

2

DLocal Limited

Consolidated Statements of Changes in Equity

Years ended December 31, 2021, 2020 and 2019

(All amounts in thousands of U.S. Dollars except share data or as otherwise indicated)

|

|

Notes |

|

Member |

|

|

Share |

|

|

Share |

|

|

Capital |

|

|

Other Reserves |

|

|

Retained |

|

|

Total |

|

|

Non- |

|

|

Total |

|

|||||||||

Balance as of January 1st, 2021 |

|

|

|

|

— |

|

|

|

602 |

|

|

|

— |

|

|

|

12,582 |

|

|

|

119 |

|

|

|

31,749 |

|

|

|

45,052 |

|

|

|

(4 |

) |

|

|

45,048 |

|

Comprehensive Income for the year |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|||||||||

Profit of the year |

|

|

|

|

— |

|

|

|

— |

|

|

|

— |

|

|

|

— |

|

|

|

— |

|

|

|

77,876 |

|

|

|

77,876 |

|

|

|

(23 |

) |

|

|

77,853 |

|

Exchange difference on translation on foreign |

|

|

|

|

— |

|

|

|

— |

|

|

|

— |

|

|

|

— |

|

|

|

(149 |

) |

|

|

242 |

|

|

|

93 |

|

|

|

9 |

|

|

|

102 |

|

Total Comprehensive Income for the year |

|

|

|

|

— |

|

|

|

— |

|

|

|

— |

|

|

|

— |

|

|

|

(149 |

) |

|

|

78,118 |

|

|

|

77,969 |

|

|

|

(14 |

) |

|

|

77,955 |

|

Transactions with Group owners in their |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|||||||||

Initial public offering, net of underwriting discount |

|

13 |

|

|

— |

|

|

|

9 |

|

|

|

86,441 |

|

|

|

— |

|

|

|

— |

|

|

|

— |

|

|

|

86,450 |

|

|

|

— |

|

|

|

86,450 |

|

Issue of ordinary shares |

|

13 |

|

|

— |

|

|

|

45 |

|

|

|

63,132 |

|

|

|

— |

|

|

|

— |

|

|

|

— |

|

|

|

63,177 |

|

|

|

— |

|

|

|

63,177 |

|

Par value change from 1.1211 U.S. Dollars to 1 |

|

13 |

|

|

— |

|

|

|

(70 |

) |

|

|

70 |

|

|

|

— |

|

|

|

— |

|

|

|

— |

|

|

|

— |

|

|

|

— |

|

|

|

— |

|

Share-options exercise |

|

|

|

|

— |

|

|

|

— |

|

|

|

6,979 |

|

|

|

(6,898 |

) |

|

|

— |

|

|

|

— |

|

|

|

81 |

|

|

|

— |

|

|

|

81 |

|

Forfeitures |

|

|

|

|

— |

|

|

|

— |

|

|

|

— |

|

|

|

(6 |

) |

|

|

— |

|

|

|

— |

|

|

|

(6 |

) |

|

|

— |

|

|

|

(6 |

) |

Warrant excercise |

|

13 |

|

|

— |

|

|

|

4 |

|

|

|

529 |

|

|

|

(533 |

) |

|

|

— |

|

|

|

— |

|

|

|

0 |

|

|

|

— |

|

|

|

— |

|

Share-based payments |

|

9 |

|

|

— |

|

|

|

— |

|

|

|

— |

|

|

|

7,596 |

|

|

|

— |

|

|

|

— |

|

|

|

7,596 |

|

|

|

— |

|

|

|

7,596 |

|

Transactions with Group owners in their |

|

|

|

|

— |

|

|

|

(12 |

) |

|

|

157,151 |

|

|

|

159 |

|

|

|

— |

|

|

|

— |

|

|

|

157,298 |

|

|

|

— |

|

|

|

157,298 |

|

Balance as of December 31st, 2021 |

|

|

|

|

— |

|

|

|

590 |

|

|

|

157,151 |

|

|

|

12,741 |

|

|

|

(30 |

) |

|

|

109,867 |

|

|

|

280,319 |

|

|

|

(18 |

) |

|

|

280,301 |

|

Balance as of January 1st, 2020 |

|

|

|

|

602 |

|

|

|

— |

|

|

|

— |

|

|

|

5,287 |

|

|

|

14 |

|

|

|

18,460 |

|

|

|

24,363 |

|

|

|

166 |

|

|

|

24,529 |

|

Adjustments due to reorganizations |

|

|

|

|

(602 |

) |

|

|

602 |

|

|

|

— |

|

|

|

— |

|

|

|

— |

|

|

|

— |

|

|

|

— |

|

|

|

— |

|

|

|

— |

|

Adjusted balance as of January 1st, 2020 |

|

|

|

|

— |

|

|

|

602 |

|

|

|

— |

|

|

|

5,287 |

|

|

|

14 |

|

|

|

18,460 |

|

|

|

24,363 |

|

|

|

166 |

|

|

|

24,529 |

|

Comprehensive Income for the year |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|||||||||

Profit of the year |

|

|

|

|

— |

|

|

|

— |

|

|

|

— |

|

|

|

— |

|

|

|

— |

|

|

|

28,184 |

|

|

|

28,184 |

|

|

|

3 |

|

|

|

28,187 |

|

Exchange difference on translation on foreign |

|

|

|

|

— |

|

|

|

— |

|

|

|

— |

|

|

|

— |

|

|

|

105 |

|

|

|

(58 |

) |

|

|

47 |

|

|

|

(10 |

) |

|

|

37 |

|

Total Comprehensive Income for the year |

|

|

|

|

— |

|

|

|

— |

|

|

|

— |

|

|

|

— |

|

|

|

105 |

|

|

|

28,126 |

|

|

|

28,231 |

|

|

|

(7 |

) |

|

|

28,224 |

|

Transactions with Group owners in their |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|||||||||

Share-based payments |

|

9 |

|

|

— |

|

|

|

— |

|

|

|

— |

|

|

|

7,295 |

|

|

|

— |

|

|

|

— |

|

|

|

7,295 |

|

|

|

— |

|

|

|

7,295 |

|

Distribution of retained earnings |

|

13 |

|

|

— |

|

|

|

— |

|

|

|

— |

|

|

|

— |

|

|

|

— |

|

|

|

(15,000 |

) |

|

|

(15,000 |

) |

|

|

— |

|

|

|

(15,000 |

) |

Transaction between shareholders |

|

13 |

|

|

— |

|

|

|

— |

|

|

|

— |

|

|

|

— |

|

|

|

— |

|

|

|

163 |

|

|

|

163 |

|

|

|

(163 |

) |

|

|

— |

|

Transactions with Group owners in their |

|

|

|

|

— |

|

|

|

— |

|

|

|

— |

|

|

|

7,295 |

|

|

|

— |

|

|

|

(14,837 |

) |

|

|

(7,542 |

) |

|

|

(163 |

) |

|

|

(7,705 |

) |

Balance as of December 31st, 2020 |

|

|

|

|

— |

|

|

|

602 |

|

|

|

— |

|

|

|

12,582 |

|

|

|

119 |

|

|

|

31,749 |

|

|

|

45,052 |

|

|

|

(4 |

) |

|

|

45,048 |

|

Balance as of January 1st, 2019 |

|

|

|

|

— |

|

|

|

588 |

|

|

|

— |

|

|

|

238 |

|

|

|

(13 |

) |

|

|

12,858 |

|

|

|

13,671 |

|

|

|

166 |

|

|

|

13,837 |

|

Comprehensive Income for the year |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|||||||||

Profit of the year |

|

|

|

|

— |

|

|

|

— |

|

|

|

— |

|

|

|

— |

|

|

|

— |

|

|

|

15,602 |

|

|

|

15,602 |

|

|

|

— |

|

|

|

15,602 |

|

Exchange difference on translation on foreign |

|

|

|

|

— |

|

|

|

— |

|

|

|

— |

|

|

|

— |

|

|

|

27 |

|

|

|

— |

|

|

|

27 |

|

|

|

— |

|

|

|

27 |

|

Total Comprehensive Income for the year |

|

|

|

|

— |

|

|

|

— |

|

|

|

— |

|

|

|

— |

|

|

|

27 |

|

|

|

15,602 |

|

|

|

15,629 |

|

|

|

— |

|

|

|

15,629 |

|

Transactions with Group owners in their |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|||||||||

Share-based payments |

|

9 |

|

|

— |

|

|

|

— |

|

|

|

— |

|

|

|

5,049 |

|

|

|

— |

|

|

|

— |

|

|

|

5,049 |

|

|

|

— |

|

|

|

5,049 |

|

Distribution of retained earnings |

|

13 |

|

|

— |

|

|

|

— |

|

|

|

— |

|

|

|

— |

|

|

|

— |

|

|

|

(10,000 |

) |

|

|

(10,000 |

) |

|

|

— |

|

|

|

(10,000 |

) |

Issue of ordinary shares |

|

13 |

|

|

— |

|

|

|

14 |

|

|

|

— |

|

|

|

— |

|

|

|

— |

|

|

|

— |

|

|

|

14 |

|

|

|

— |

|

|

|

14 |

|

Transactions with Group owners in their |

|

|

|

|

— |

|

|

|

14 |

|

|

|

— |

|

|

|

5,049 |

|

|

|

— |

|

|

|

(10,000 |

) |

|

|

(4,937 |

) |

|

|

— |

|

|

|

(4,937 |

) |

Balance as of December 31st, 2019 |

|

|

|

|

— |

|

|

|

602 |

|

|

|

— |

|

|

|

5,287 |

|

|

|

14 |

|

|

|

18,460 |

|

|

|

24,363 |

|

|

|

166 |

|

|

|

24,529 |

|

The accompanying notes are an integral part of these consolidated financial statements.

3

DLocal Limited

Consolidated Statements of Cash Flows

Years ended December 31, 2021, 2020 and 2019

(All amounts in thousands of U.S. Dollars except share data or as otherwise indicated)

|

|

Notes |

|

2021 |

|

|

2020 |

|

|

2019 |

|

|||

Cash flows from operating activities |

|

|

|

|

|

|

|

|

|

|

|

|||

Profit before income tax |

|

|

|

|

85,500 |

|

|

|

31,418 |

|

|

|

17,823 |

|

Adjustments: |

|

|

|

|

|

|

|

|

|

|

|

|||

Interest income from financial instruments |

|

|

|

|

(2,556 |

) |

|

|

(443 |

) |

|

|

(217 |

) |

Interest charges for lease liabilities |

|

|

|

|

142 |

|

|

|

20 |

|

|

|

30 |

|

Other finance expense / (income) |

|

|

|

|

402 |

|

|

|

(3 |

) |

|

|

(6 |

) |

Amortization of Intangible assets |

|

10 |

|

|

3,917 |

|

|

|

656 |

|

|

|

175 |

|

Depreciation of Property, plant and equipment |

|

10 |

|

|

377 |

|

|

|

155 |

|

|

|

53 |

|

Amortization of Right-of-use asset |

|

10 |

|

|

453 |

|

|

|

181 |

|

|

|

181 |

|

Revenue reduction related to prepaid assets |

|

17 |

|

|

200 |

|

|

|

67 |

|

|

|

— |

|

Share-based payment expense |

|

9 |

|

|

7,590 |

|

|

|

7,295 |

|

|

|

5,049 |

|

Net exchange differences |

|

|

|

|

(19 |

) |

|

|

(99 |

) |

|

|

(106 |

) |

Fair value (loss)/gain on financial assets at fair value through profit or loss |

|

|

|

|

16 |

|

|

|

(9 |

) |

|

|

(56 |

) |

Other operating (gain)/loss |

|

24 |

|

|

(2,896 |

) |

|

|

2,896 |

|

|

|

— |

|

Net Impairment loss/(gain) on financial assets |

|

16 |

|

|

33 |

|

|

|

(808 |

) |

|

|

807 |

|

|

|

|

|

|

93,159 |

|

|

|

41,326 |

|

|

|

23,733 |

|

Changes in working capital |

|

|

|

|

|

|

|

|

|

|

|

|||

Increase in Trade and other receivables |

|

16 |

|

|

(115,355 |

) |

|

|

(45,932 |

) |

|

|

(10,968 |

) |

Increase / (Decrease) in Other assets |

|

17 |

|

|

581 |

|

|

|

(1,114 |

) |

|

|

(1,113 |

) |

Increase in Trade and other payables |

|

21 |

|

|

134,295 |

|

|

|

89,888 |

|

|

|

20,284 |

|

Increase in Tax Liabilities |

|

23 |

|

|

5,309 |

|

|

|

5,877 |

|

|

|

— |

|

Increase in Provisions |

|

25 |

|

|

317 |

|

|

|

595 |

|

|

|

497 |

|

Cash from operating activities |

|

|

|

|

118,306 |

|

|

|

90,640 |

|

|

|

32,433 |

|

Income tax paid |

|

12 |

|

|

(9,820 |

) |

|

|

(2,154 |

) |

|

|

(1,710 |

) |

Net cash from operating activities |

|

|

|

|

108,486 |

|

|

|

88,486 |

|

|

|

30,723 |

|

Cash flows from investing activities |

|

|

|

|

|

|

|

|

|

|

|

|||

Acquisitions of Property, plant and equipment |

|

|

|

|

(1,949 |

) |

|

|

(876 |

) |

|

|

(152 |

) |

Additions of Intangible assets |

|

20 |

|

|

(46,068 |

) |

|

|

(3,006 |

) |

|

|

(1,554 |

) |

Net collections of financial assets at FVPL |

|

|

|

|

7,520 |

|

|

|

7,089 |

|

|

|

1,601 |

|

Interest collected from financial instruments |

|

|

|

|

2,556 |

|

|

|

443 |

|

|

|

217 |

|

Other finance income collected |

|

|

|

|

— |

|

|

|

— |

|

|

|

6 |

|

Net cash (used in) / provided by investing activities |

|

|

|

|

(37,941 |

) |

|

|

3,650 |

|

|

|

118 |

|

Cash flows from financing activities |

|

|

|

|

|

|

|

|

|

|

|

|||

Proceeds from issuance of shares |

|

13 |

|

|

63,177 |

|

|

|

— |

|

|

|

14 |

|

Proceeds from initial public offering |

|

1.3 |

|

|

87,088 |

|

|

|

— |

|

|

|

— |

|

Initial public offering expenses paid |

|

|

|

|

(638 |

) |

|

|

— |

|

|

|

— |

|

Share-options exercise |

|

|

|

|

81 |

|

|

|

— |

|

|

|

— |

|

Dividends paid |

|

|

|

|

— |

|

|

|

(15,000 |

) |

|

|

(10,000 |

) |

Proceeds from borrowings |

|

|

|

|

5,000 |

|

|

|

— |

|

|

|

— |

|

Interest payments on lease liability |

|

|

|

|

(142 |

) |

|

|

(20 |

) |

|

|

(30 |

) |

Principal payments on lease liability |

|

29 |

|

|

(430 |

) |

|

|

(131 |

) |

|

|

(152 |

) |

Payments of loans advanced to shareholders |

|

|

|

|

— |

|

|

|

— |

|

|

|

(9,174 |

) |

Other finance expense paid |

|

|

|

|

(388 |

) |

|

|

(47 |

) |

|

|

— |

|

Net cash provided by / (used in) financing activities |

|

|

|

|

153,748 |

|

|

|

(15,198 |

) |

|

|

(19,342 |

) |

Net increase in cash flow |

|

|

|

|

224,293 |

|

|

|

76,938 |

|

|

|

11,499 |

|

Cash and cash equivalents at the beginning of the year |

|

|

|

|

111,733 |

|

|

|

34,765 |

|

|

|

23,305 |

|

Effects of exchange rate changes on cash and cash equivalents |

|

|

|

|

171 |

|

|

|

30 |

|

|

|

(39 |

) |

Cash and cash equivalents at the end of the year |

|

|

|

|

336,197 |

|

|

|

111,733 |

|

|

|

34,765 |

|

The accompanying notes are an integral part of these consolidated financial statements.

4

DLocal Limited

Notes to the Consolidated Financial Statements

At December 31, 2021

(All amounts in thousands of U.S. Dollars except share data or as otherwise indicated)

1.1 General information

DLocal Limited (“dLocal” or the “Company”) is a holding company, referred to together with its subsidiaries as the “Group”. dLocal is a limited liability company. The Group was established on October 5, 2016, under the holding company dLocal Group Limited, domiciled and incorporated in Malta, and on April 14, 2021 it was reorganized under dLocal, domiciled and incorporated in the Cayman Islands. The Company is the ultimate controlling party of the Group. See detail of subsidiaries in Note 4: Consolidation of subsidiaries.

The Group processes online payment transactions through more than 700 payment methods on December 31, 2021 and 2020, enabling enterprise merchants located in developed economies (mainly United States, Europe and China) to get paid (“payins”) from customers in emerging markets and to make payments (“payouts”) to customers in emerging markets. As of the date of issuance of this Consolidated Financial Statements, the Group continued to focus on its expansion efforts bringing the total number of countries in the geographic network to 35.

In order to conduct its business, the Group has direct connections with banks, acquirers and payments processors to process payments locally in emerging markets. It also operates with financial institutions to expatriate/repatriate the funds to/from the developed economies where the merchant customers elect to settle their funds in the currency of their preference (mainly U.S. Dollar and Euro). These consolidated financial statements include dLocal’s subsidiaries and details of the structure are included under Note 4: Consolidation of subsidiaries.

The Group is licensed and regulated in the EU as an Electronic Money Issuer, or EMI, and Payment Institution, or PI, and registered as a Money Service Business with the Financial Crimes Enforcement Network of the U.S. Department of the Treasury, or FinCEN, and we operate and are licensed, as applicable, in more than 25 countries in emerging markets, primarily in the Americas, Asia and Africa.

In addition, the Group is subject to laws aimed at preventing money laundering, corruption and the financing of terrorism. This regulatory landscape is constantly changing, including as a consequence of the implementation of the Fourth Anti-Money Laundering Directive (Directive 2015/849/EU, “MLD4”) and the proposed amendments to the MLD4, often referred to as the fourth Anti-Money Laundering Directive.

As part of the requirements for maintaining its financial institution license, the subsidiary dLocal Limited is subject to externally imposed capital requirements by the regulator, which initially amounted to Euros 400 (USD 453). As at 31 December 2021 the subsidiary calculated its capital requirement at the level of Euros 530 (USD 600). As at 31 December 2021 Tier 1 Capital was temporarily short in respect of its regulatory capital requirement with an amount of USD 37,666. Such position will be rectified upon the signing of the subsidiary's financial statements, due to the fact that profits registered during the year ended 31 December 2021 will be verified as a result of the external audit of the financial statements of the subsidiary, and Tier 1 Capital post verification will be considered to be that of USD 4,621, which is in excess of the externally imposed minimum capital requirement of Euros 530 (USD 600).

1.2 Reorganization

On April 14, 2021, in a series of transactions as further described below, the owners of dLocal Group Limited completed the contribution of 100% of their respective interests in dLocal Group Limited, with par value 1.1211 U.S. Dollars per share, on a pro rata basis to a newly formed entity, dLocal, in exchange for 100% of the common shares of dLocal, with par value 1 U.S. Dollars per share with no additional consideration, is defined as the “Reorganization”. The purpose of the Reorganization was to facilitate the initial public offering of the Group. dLocal had no prior assets, holdings or operations.

In connection with the Reorganization, the Group amended its existing employee share incentive plan, the “2020 Global Share Incentive Plan”. In this context, all obligations of dLocal Group Limited under this plan (including award agreements issued thereunder) have been transferred to dLocal, and options to purchase ordinary shares of dLocal Group Limited have been converted into options to purchase ordinary shares of dLocal. The conversion was based on a ratio intended to maintain in all material respects the same, and in no event greater, economic benefit to optionees as provided under the plans in effect prior to the Reorganization.

5

Additionally, the written resolution of dLocal’s shareholders dated May 19, 2021 and effective June 2, 2021, approved a 500-for-1 stock split of dLocal’s common shares, whereby every share of capital stock of dLocal was converted into 500 shares, changing the par value of dLocal’s common shares from 1 U.S. Dollars to 0.002 U.S. Dollars. Therefore, dLocal increased total shares outstanding from 577,008 shares to 288,504,000 shares. Consequently the 2020 Global Share Incentive Plan was also amended to reflect such change in the par value of the common shares. References made to outstanding shares and per share amounts in the accompanying financial statements and applicable disclosures have been retroactively adjusted to reflect this stock split.

The Reorganization was limited to entities which were all under the control of the same shareholder group and was implemented in part to facilitate the IPO, it did not qualify as a business combination under common control; rather, it was a Reorganization of the capital of dLocal Group Limited, the existing organization. Therefore, all financial and other information herein relating to December 2020 and 2019 are presented using the historical values from the consolidated financial statements of dLocal Group Limited. However, the issued share capital reflects that of Dlocal as of the Reorganization date.

1.3 Significant events during the year

a) Filing of Form S-8

Effective November 26, 2021, the Company filed a Form S-8 with the SEC, which allows dlocal to register securities it offers as part of its employee benefit plan.

b) Secondary offering

On October 25, 2021 the Company announced the closing of an underwritten public offering of 17,000,000 Class A common shares which were sold by certain selling shareholders at a public offering price of USD 52.25 per share. The offering was made pursuant to a registration statement on Form F-1 filed with the U.S. Securities and Exchange Commission (“SEC”). This public offering was secondary for which the Company did not receive any cash in exchange of shares.

In connection with the offering, the selling shareholders have granted the underwriters the option to purchase up to 2,550,000 additional Class A common shares at the public offering price less the underwriting discounts and commissions.

See Note 8.iv).

c) Warrant exercise

On September 2, 2021 a holder of warrants exercised its net issuance right resulting in a net issuance on September 7, 2021 of 2,112,676 shares at a Fair Market Value of U.S. Dollars 65.14 per share, calculated using the average price of 5 business days before the exercise date.

d) Initial Public Offering (IPO)

On June 3, 2021, the Company successfully completed an initial public offering of its shares on the Nasdaq Global Select Market. The Company issued 4,411,765 shares, at a price of 21 U.S. Dollars per share prior to the underwriting discount of 6%. In addition, on June 3, 2021 the over-allotment option was exercised by the underwriters of the initial public offering on a secondary offering.

e) Acquisition of certain assets from PrimeiroPay

On March 11, 2021, dLocal signed a contract to acquire certain assets (mainly merchant agreements) from Primeiropay S.A.R.L and PrimeiroPay Technology GmbH (“Primeiropay”) in accordance to the Transfer of a Going Concern Agreement signed between the parties. The purchase of this acquisition of assets amounted to 40 million U.S. Dollars, of which 1.33 million U.S. Dollars is contingent consideration (subject to the achievement of the “earn-out”) and 38.67 million U.S. Dollars was an immediate cash consideration, with an effective date of April 1, 2021. On August 31, 2021 the earn-out period finalized and the earn-out conditions were not achieved. However, the merchant contracts migration from Primeiropay to Dlocal is in progress, as a consequence the recognized contingent liability, capped in USD 665 thousands, is expected to be paid conditioned to finalizing the migration process estimated during 2022.

Primeiropay is an international payment service provider that delivers payment services for international merchants that want to accept payments from their international customers without setting up a local entity through processing all cards and payment methods domestically in local currencies. The concentration test outlined on IFRS 3 was met and therefore the transaction was classified as an asset acquisition. For further details refer to Note 20: Intangible assets.

6

f) Loan related to Employee share purchase plan (ESPP)

In November 2020 dLocal Group Limited signed a non-recourse “Loan Agreement” with two officers to fund the acquisition of shares under the ESPP.

During March and April 2021, dLocal received payments for USD 31,644 (equivalent to 15,459,000 common shares) that were considered as the collection of the exercise price of the options under the ESPP for the issuance of shares. Therefore, dLocal recognized for such collections the cash inflow against equity. As of the date of issuance of this Consolidated Financial Statements, the loan and the corresponding accrued interest had been fully repaid.

g) Coronavirus pandemic

As of the date of these Consolidated Financial Statements, the impact of the COVID-19 pandemic on our operations has had a different impact across our different product offerings and the different verticals the Group serves, with certain industries benefiting from increased adoption (e.g., retail, streaming, gaming, social media) while others suffering initially from decreased usage (e.g., travel, ride hailing), however subsequently recovered to its pre pandemic volumes.